Revisiting: Unimech Aerospace

Immense tailwinds, but need a close watch on execution

Continuing from the previous post:

Unimech Aerospace & Manufacturing operates in

(1) Aero Tooling/MRO tooling: This is 85% of their business at this stage. Aero engine tools for LEAP, Pratt & Whitney, and Rolls-Royce engines; Airframe tools for Airbus & Boeing.

(2) Precision Components and Assemblies: 15% of revenue. Precision parts and assemblies for Nuclear, Aero, Defence, and other Emerging Industries.

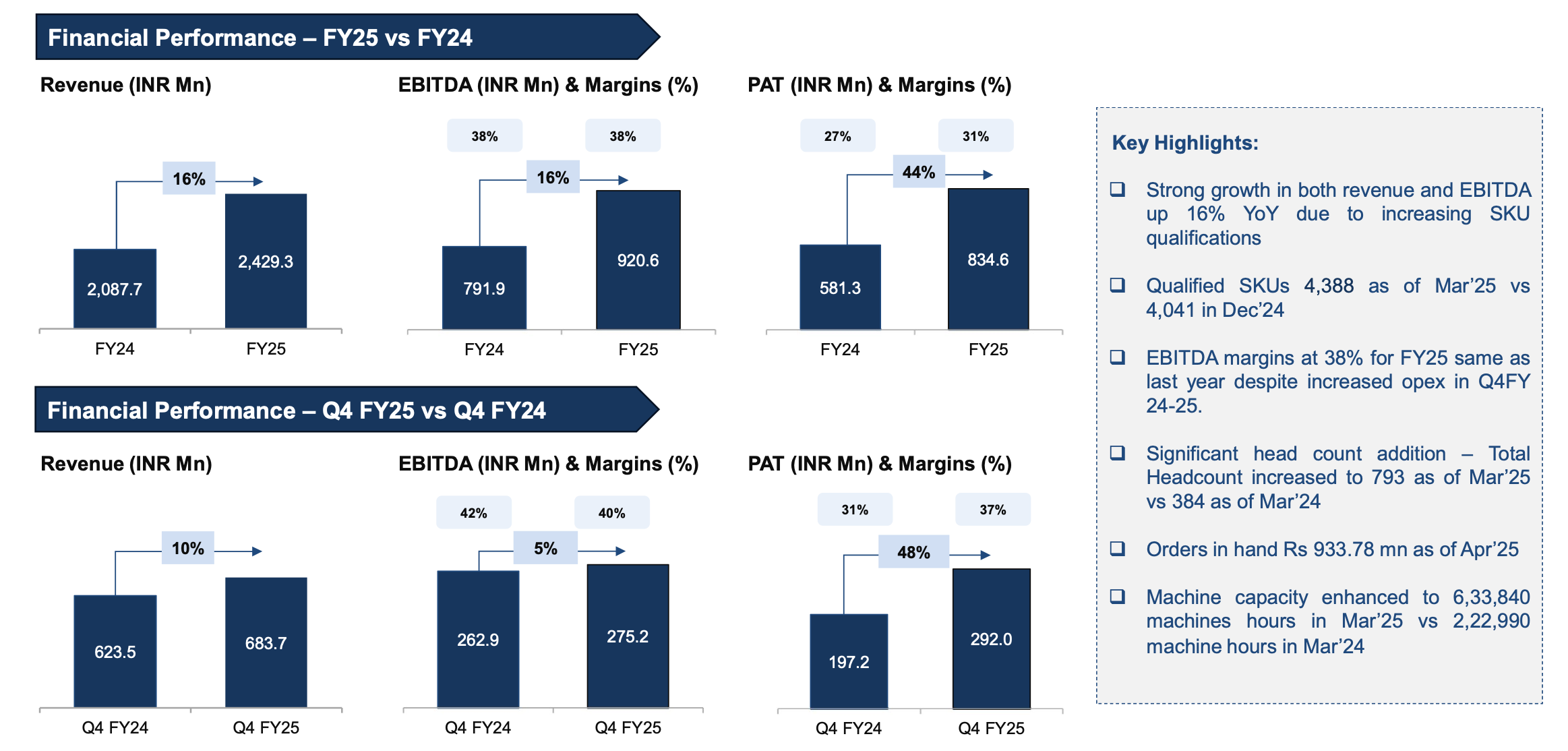

(1) FY2025 Results

Only 16% growth. Given the hefty valuation (looking at the PE metric), this growth gives nothing to cheer.

The relatively higher profit growth (compared to EBITDA) is mainly due to other income from investments (IPO proceeds) and hence is not core growth.

There has been a significant capacity addition in FY25, which gives room for 3 years of growth.(2) But the market reaction was completely different

Technically, it broke out strongly.

It is a case study on gaps as well as on support and resistance.

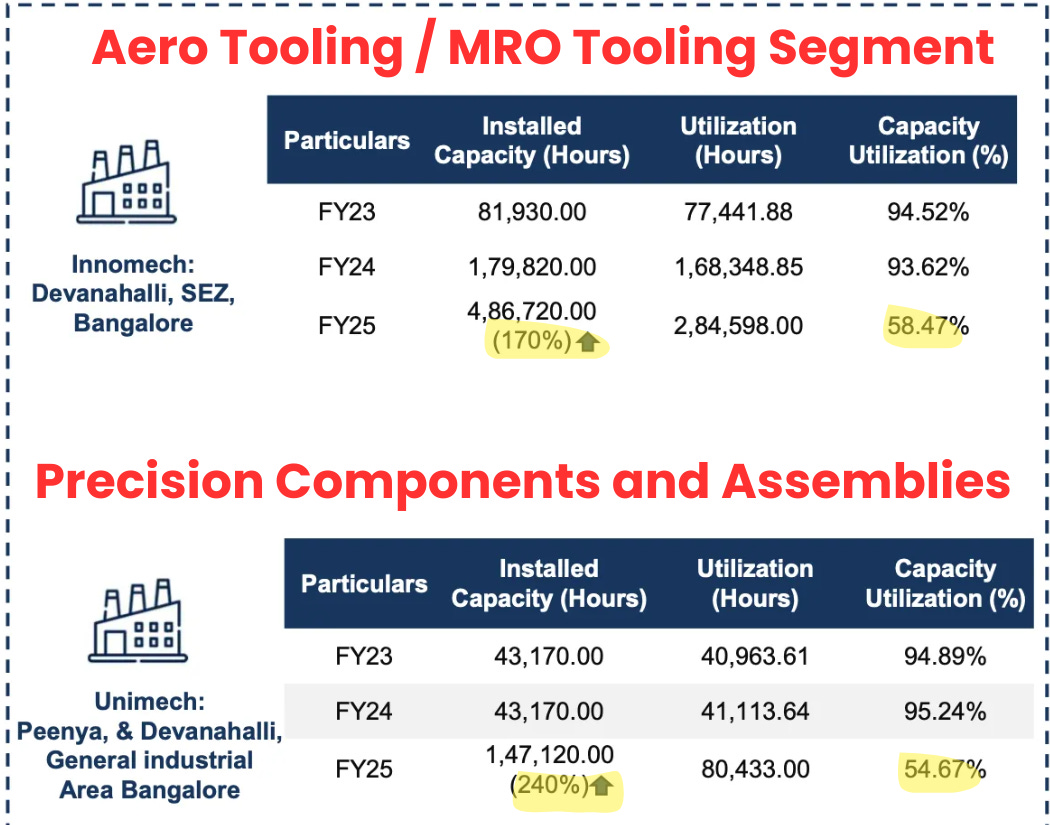

Look how the area that was once a resistance zone turned into support.(3) Huge Capacity Addition

Capacity has been increased in a step function.

Utilisation has dropped to ~55-58% levels

Case for operating leverage in the future as they increase their utilization. As per management, they expect to reach ~85% capacity utilization in 3 years.

(4) Sector Tailwinds - Engine Development

After the Op Sindoor, there is renewed attention and a push towards Atmanirbharta. The strategic areas need indigenous systems, subsystems, parts, and materials. An area of strategic advancement for India to enhance the defence forces is the Engine Development for indigenous Air Force Assets (Fighters, Helis, UAVs, etc)

An important development is the approval of the AMCA programme. It is important to note that Private Industry is being given equal opportunity

Press Release: https://www.pib.gov.in/PressReleasePage.aspx?PRID=2131528

A key challenge for Indian Aircraft is the Jet Engine. Clarity will emerge in due course on whether we are moving ahead with indigenous engine development or with a foreign collaboration, or whether two to three different programmes will go parallel.

Whatever the case, Unimech can support the programme in providing tooling or precision parts. Domestic Private Players will be an integral part of this programme.Strategic partnership

Exclusive manufacturing agreement for the production of micro gas turbine engines developed by Dheya and manufactured by Unimech, including orders for sub-systems.

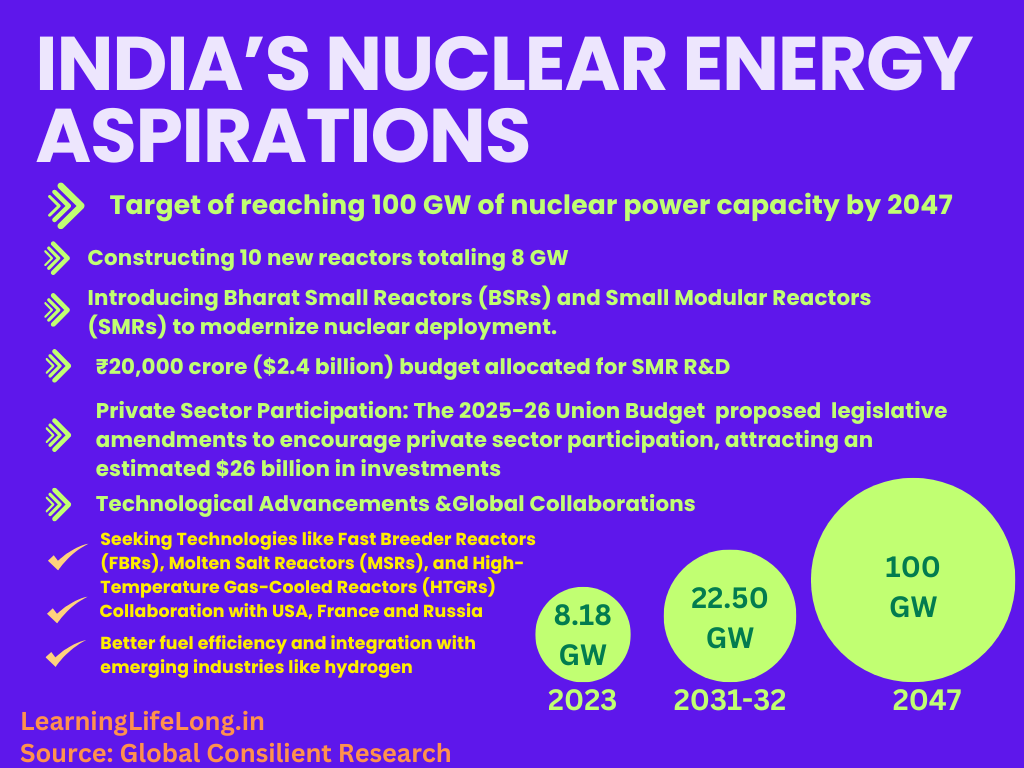

Frankly, this area needs more research on how capable Dheya themselves are and what the opportunity could be for Unimech. They have a roadmap for a 30% stake in Dheya.(5) Sector Tailwinds - Nuclear Energy

IMO, the principles behind the Energy Policies across the globe are changing. The pecking order for policy objectives seems to be

Energy Security > Economic Efficiency > Environmental ConcernsWith this quest for security, an important part of the Energy Mix is going to be Nuclear. I’ve alluded to this in the post on SMRs.

Q4 Concall: NPCIL planning 11 new reactors. Each reactor budget is above 1000 cr; Unimech plans to participate in 15 subsystems - an opportunity of 400cr in each reactor. Plus, there will be opportunities in SMRs.(6) Sector Tailwinds - India’s growing Passenger Aviation Market - Commercial Sector MRO

India has become the 3rd largest passenger aircraft market. The MRO sector is expected to grow from US$ 1.7 Bn in 2021 to US$ 4 Bn by 2031. (Niti Aayog report cited in concall)

Engine MRO is a moated space - they work with both LEAP and Rolls-Royce EnginesTailwinds are great, but execution is paramount. Valuations don’t leave any room for error.

The guidance for FY2026 is a 40% growth. Currently, the company is export-heavy, and that too to the United States.

With the US, there is a lot of uncertainty about tariffs. Plus, the policy on high-tech sectors is very unpredictable. Management itself expects Q1 and Q2 to be slow.Currently, the mix between Aero Tooling/MRO to Precision Component Segment is 85:15. Precision Component has relatively lesser margins. Going forward, growth in precision will outpace Aero Tooling/MRO

Although they don't want to go below 35% EBITDA margins. The business mix change will put a relative pressure on the margin.

Disclaimer: At this stage, this is a technical bet for me. There are too many moving parts. The taiwinds are immense, but given the kind of industry they are in, I think it will take time to materialize.

*****

Invest in yourself…. be a learning machine.

These communities have helped me learn the nuances of investing. Why not check them out? - Join the community of learners.

Free Course by Vivek Mashrani

Supporting my work

This Substack will never be paywalled. I don’t want to accept voluntary payments for future unknown work.

But if you got this far, chances are you find my writing valuable. So please spread the word! Sharing, liking, and commenting all help spread the word!

Connect on X @pankajgarg_ciet

Disclaimer: Views are personal. I am not SEBI registered. The information provided here is for educational purposes only. This is not buy or sell advice. I will not be responsible for any of your profit/loss based on the above information. Consult your financial advisor before making any decisions.