Exicom Tele Systems

Can it become AI DC Proxy?

TLDR

The market is pricing Exicom as an EV-charger turnaround story. Buried in its Q4 FY26 investor deck is something else entirely: a 1.6MW, 800–950V DC bi-directional inverter, sitting inside a hyperscaler’s test programme. This is an analysis of that optionality.

The core EV charging opportunity is structurally external to automakers - EV OEMs will outsource this.

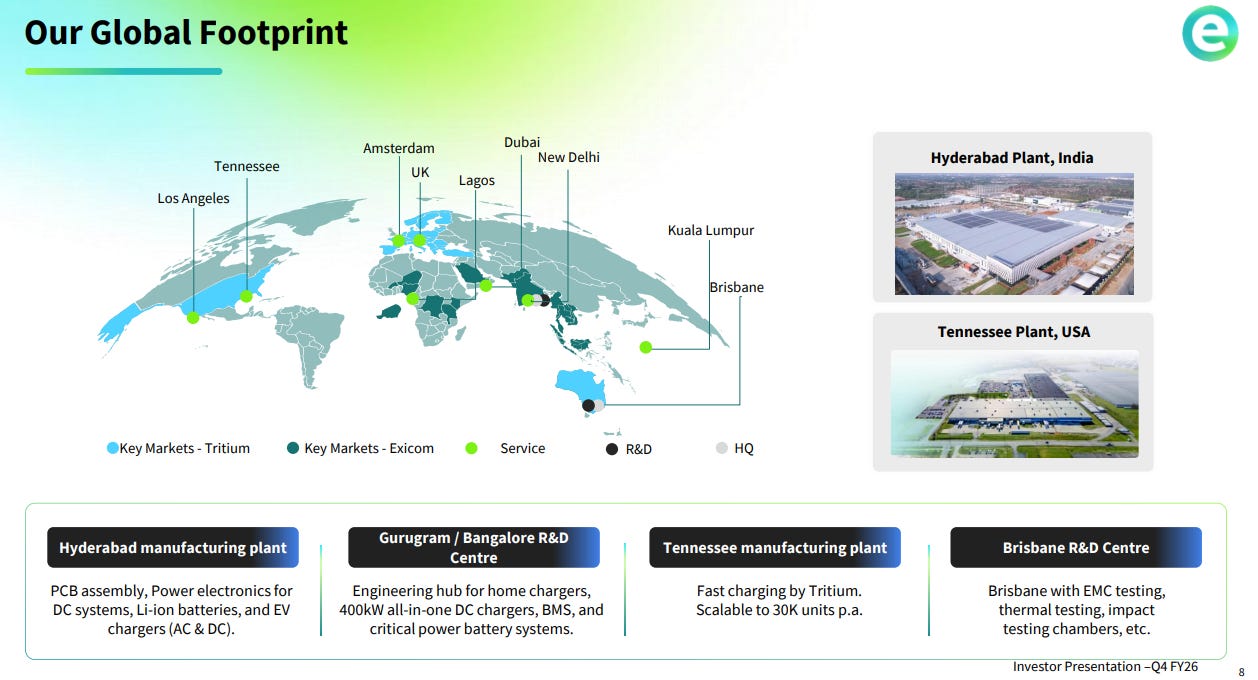

Exicom bought Tritium out of insolvency for ~$37Mn in 2024 — inheriting a BABA-compliant (Build America, Buy America Act) Tennessee plant, a 13,000-unit installed base in 47 countries, and a Brisbane engineering team that has run 950V DC systems commercially since 2018.

Tritium is inflecting: Q4 FY26 revenue of $9.7Mn (+157% QoQ), $12.6Mn backlog, EBITDA breakeven targeted by Q4 FY27.

The hidden option is GRID-FLEX — a 800–950V DC bi-directional inverter for datacenters and BESS, launched Dec 2025, built on the same 50kW liquid-cooled modules as Tritium’s EV chargers, already in Factory Acceptance Testing (FAT) with a global hyperscaler - which is a binary catalyst putting Exicom on the AI/DC proxy map.

High Risk Story - Turnarounds are difficult to execute.

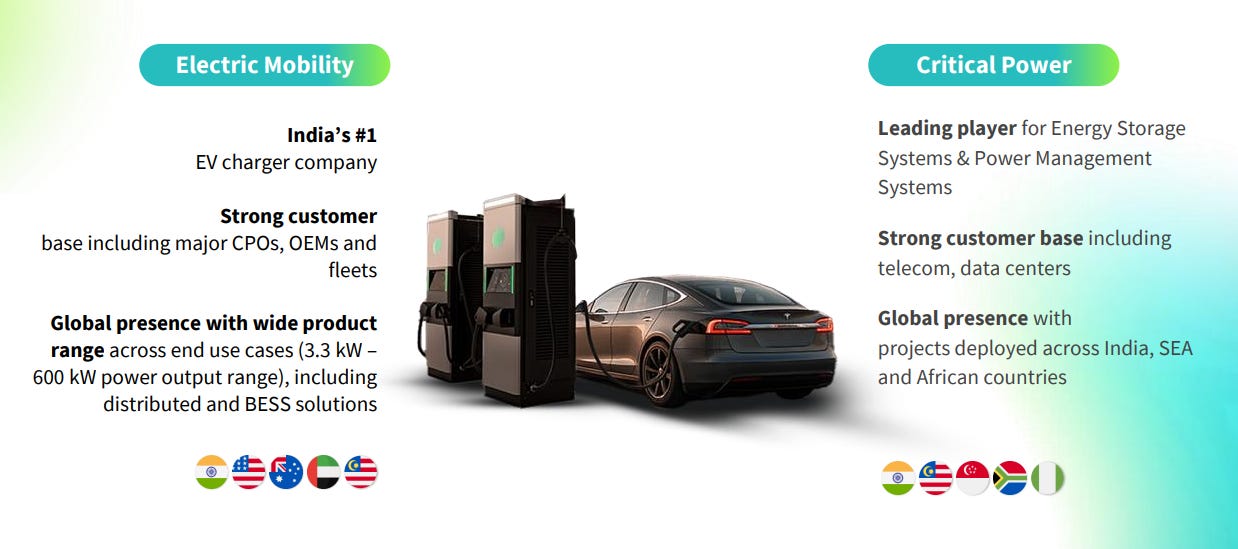

Exicom

Exicom itself runs two businesses.

Critical Power

DC power systems, rectifiers, Li-ion batteries for telecom and enterprise infrastructure - is the legacy cash engine, currently working through a soft telecom capex cycle but exiting FY26 with a landmark DC power systems order from a major Indian telco and record exports to Africa, the Middle East, and Southeast Asia.

EV Charging

Its growth engine, spanning India AC/DC chargers and, since the acquisition, Tritium’s global DC fast-charging franchise.

With a global footprint

FY26 closed with standalone revenue of ~₹895 crore (+19% YoY) and consolidated revenue of ~₹1,152 crore (+33% YoY). Standalone basis the company is EBITDA positive with an EBITDA of ~₹70 crore, however, the consolidated picture still carries Tritium’s turnaround costs: a consolidated EBITDA loss of ~₹103 crore and PAT loss of ~₹274 crore for the year!!

March 2026, Exicom inaugurated its ₹216 crore Hyderabad plant, a 2.5x capacity expansion.

Tritium Acquisition

In August 2024, Exicom did something most Indian mid-caps would never attempt: it bought a bankrupt Nasdaq-listed Australian company for roughly $37 million. Tritium had filed for voluntary administration in April 2024 - a casualty of cash burn, a frozen US NEVI subsidy programme, and a capital structure that could not survive the wait.

Exicom acquired the business through a Netherlands holding entity (Exicom Power Solutions B.V.), with the transaction completing through late 2024, and inherited three things of real value:

A BABA-compliant manufacturing plant in Lebanon, Tennessee with ~30,000-unit annual capacity

An installed base of ~13,000 DC fast chargers across 47 countries, and

The part almost nobody priced - one of the world’s deepest engineering benches in high-voltage DC power electronics, sitting in Brisbane.

How is the turnaround shaping?

Q4 FY26 was Tritium’s strongest commercial quarter under Exicom ownership: $9.7Mn revenue, up 157% QoQ, with a $12.6Mn backlog entering Q1 FY27, and consolidated EBITDA touching breakeven for the first time.

Management has guided Tritium to EBITDA breakeven by Q4 FY27.

Why automakers will never build this in-house

Before getting to the datacenter option, the base case deserves its own structural argument - because the most common bear question on any charger OEM is: “Won’t the car companies just do this themselves?” My view is a firm no. Charging hardware is, and will remain, an external opportunity. This is not an opinion about intent; it is an observation about revealed behaviour, economics, and competency. The automakers have already run this experiment several times, with their own money.

Case Study 1: When automakers wrote the cheque, they still bought from Tritium

Ionity is the cleanest natural experiment available. BMW, Mercedes-Benz, Ford, Hyundai, and the Volkswagen Group pooled capital in 2017 to build Europe’s high-power charging backbone.

If vertical integration into charging hardware were ever going to happen, it would have happened here: five OEMs, shared capex, a captive demand base. Instead, Ionity ran a procurement process and Tritium won it, becoming the network’s largest hardware supplier with its 350kW liquid-cooled chargers across roughly 220 of the first 400 planned sites, beating ABB. Ionity later broadened its supplier base to Alpitronic. At no point did any of the five owners propose manufacturing the chargers themselves.

North America is rerunning the same experiment with the same design. IONNA the joint venture of eight automakers including BMW, GM, Honda, Hyundai, Kia, Mercedes-Benz, Stellantis and Toyota is targeting 30,000 high-power charge points by 2030, with around 107 stations and over 1,000 stalls live as of April 2026. It is, again, a network operator and procurement vehicle, not a factory. Electrify America, Volkswagen’s $2bn dieselgate-funded network, follows the identical pattern i.e. OEM capital, third-party hardware.

This reveals that the preference is unanimous: carmakers will fund chargers, operate networks, even brand the customer experience but on 3rd party hardware.

Case Study 2: the one automaker that did integrate tried to walk away

Tesla is the exception that proves the rule. It is the only OEM that is genuinely vertically integrated by designing, manufacturing and operating its Supercharger hardware. And in April 2024, Tesla abruptly dismantled most of its roughly 500-person Supercharger organisation, pausing network expansion before partially rebuilding the team under pressure.

Even for the most vertically integrated EV maker on earth, with the world’s best charging network, the hardware-and-network business was the first thing sacrificed when capital discipline tightened. Meanwhile, the rest of the industry’s response to its charging problem was not to build factories but to adopt NACS (North American Charging System) and lease access to Tesla’s network. Faced with the choice between internalising charging and outsourcing it, every single OEM chose outsourcing, including, briefly, from Tesla itself.

Case Study 3: VinFast in India - even an OEM that owns a charging company outsources

VinFast a Vietnam based vertically integrated EV Company has begun local vehicle manufacturing in Tamil Nadu, India. Its Vingroup sibling V-Green operates roughly 150,000 charging ports in Vietnam.

It could have made a strong sense to bring charging infra as well in-house in India. Instead, V-Green signed its first co-branded CPO partnership in India with ChargeZone — V-Green handles site identification and planning, while ChargeZone owns end-to-end deployment, operations and maintenance, with 15 co-branded stations already live and nearly 100 more planned within six months.

ChargeZone itself operates one of India’s largest networks, with over 13,500 charging points across 1,200-plus locations in India and the UAE — and is an established hardware partner of Exicom, with a publicly announced partnership to deploy high-power, renewable-integrated charging stations.

So an OEM, that literally owns a charging company, rented local execution from a CPO, and the CPO layer procures hardware from specialist manufacturers.

So every Vinfast sold creates network effect for Exicom.

Why the economics force this outcome

Competency mismatch. A 350kW liquid-cooled DC fast charger is industrial power electronics: high-voltage DC conversion, thermal engineering, grid interconnection, 99%+ network uptime obligations. None of this lives inside an automotive manufacturing system, which is optimised for high-volume mechanical assembly. The skills sit in companies like Tritium, Alpitronic, Kempower, ABB and Delta — not in Wolfsburg or Detroit.

Capital allocation reality. Most legacy OEMs lose money on every EV they sell. Charging hardware is a lower-margin, capex-heavy, slow-payback business. Boards that are cutting EV programmes will not simultaneously fund charger factories and they haven’t.

Utilisation economics reject captivity. A charger earns its return on utilisation, and utilisation demands brand-agnosticism. Every OEM-built network, including Tesla’s, has ended up opening to all vehicles. An asset that must serve every brand naturally sits outside any one brand. The structure of the asset itself pushes the opportunity external.

Scale mismatch. Global DC fast-charger volumes are measured in the tens of thousands of units annually, a rounding error against automotive production volumes, yet demanding dedicated engineering and certification. Too small to matter inside an OEM; exactly the right size to be a specialist’s whole business.

The same logic, already proven in India

India compressed this entire lesson into one company’s filings. Exicom built a commanding position in Indian residential charging roughly 60% market share at the time of its IPO disclosures - almost entirely through chargers bundled and supplied at the point of sale by the car OEMs themselves. Tata, MG, Mahindra did not set up charger plants; they put Exicom’s box in the boot of the car. On the public charging side, Indian OEMs partner with charge point operators and buy hardware from specialists. The pattern is identical to Ionity and IONNA, just earlier in the curve - and India’s DC fast-charging buildout is still in front of us, now to be served from a Hyderabad plant with 2.5x the capacity.

The implication for the investment case is simple but important: the addressable market for a specialist charger OEM is the entire market - OEM-funded networks included. There is no scenario in which automakers internalise the demand away. And Tritium carries the strongest possible proof of vendor status: when the automakers themselves were the customer, writing their own cheques at Ionity, Tritium was the supplier they chose.

Now let us move to the datacenter optionality.

AI datacenters and 800V DC

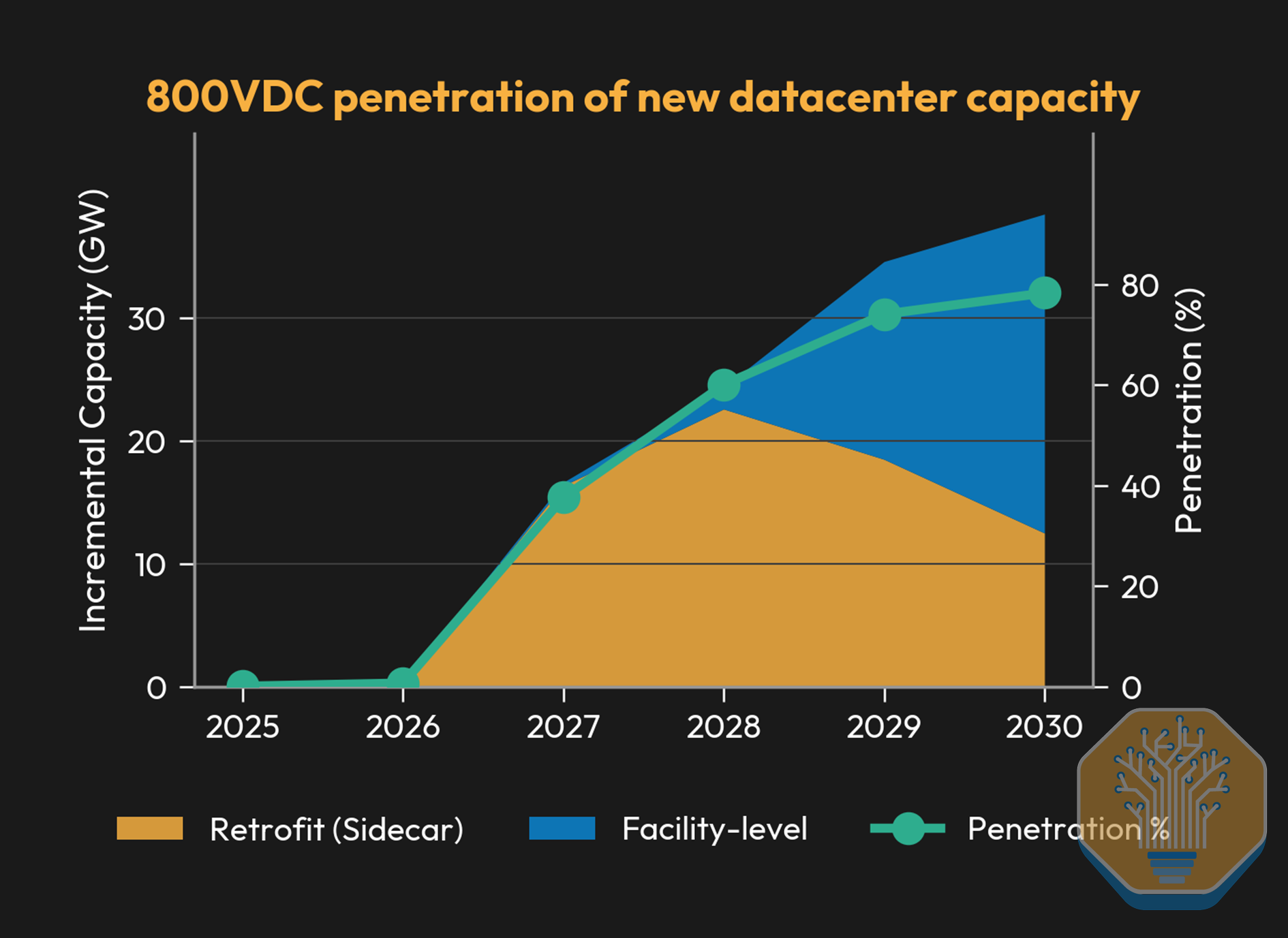

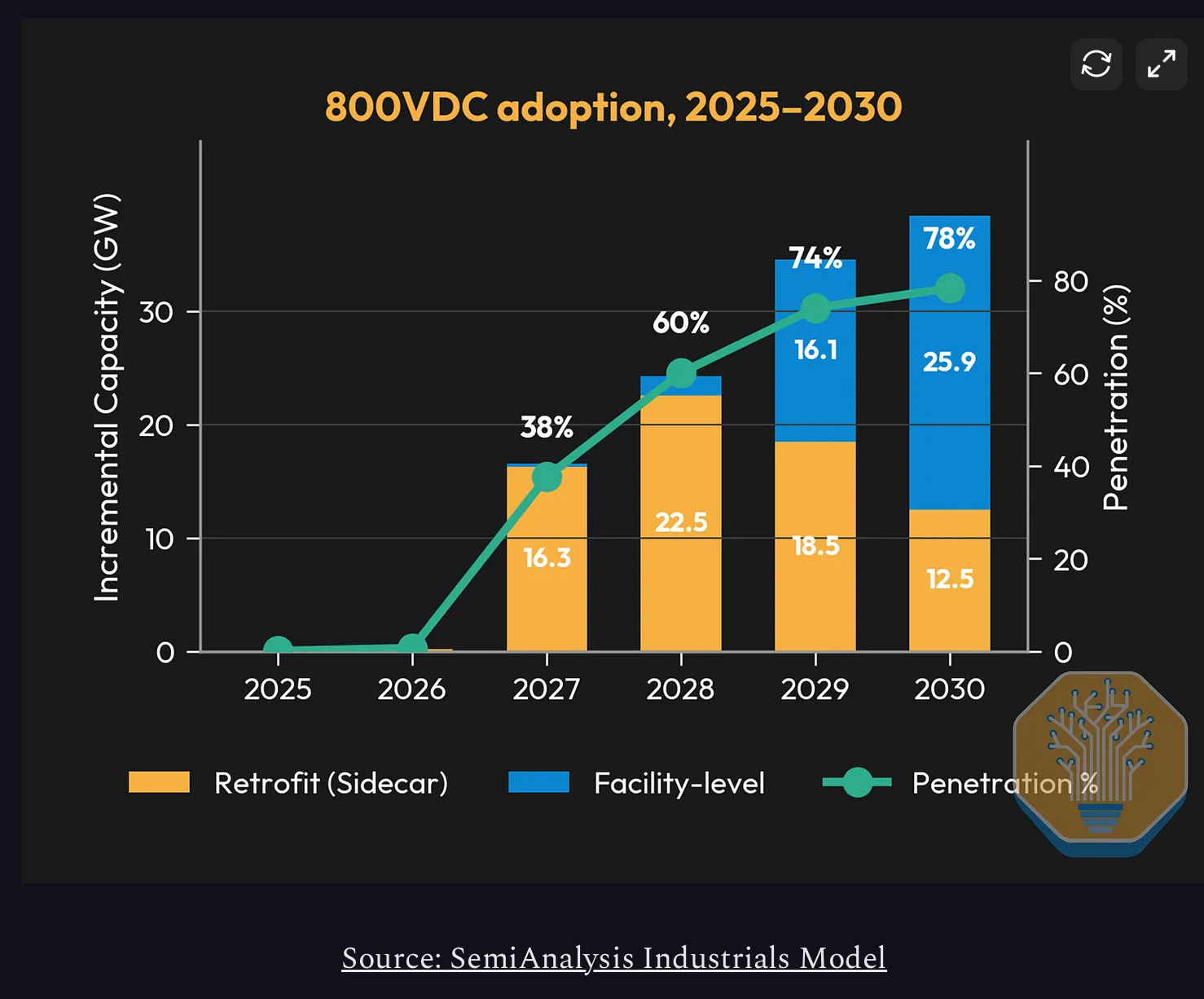

The power architecture in data centers is changing. As the power rating of GPU racks is increasing (Kyber Ultra approaching 660kW), the existing power architecture is no longer tenable.

The data centers are trending towards 800V DC power, which creates demand for power racks to power the chips

800 HVDC equipment has a lot of parallels to the EV charging industry

To understand the option, you need to understand the architectural earthquake underway in datacenter power. AI racks have blown past the limits of legacy 415V AC distribution. NVIDIA’s Rubin-class systems are pushing rack densities toward levels where copper cross-sections, conversion losses, and floor space for AC power gear all become untenable. The industry’s answer is to distribute power as ±400V to 800V direct current. Why? fewer conversion stages, smaller busbars, higher efficiency, and battery storage that couples natively to the DC bus.

NVIDIA has assembled a named partner ecosystem for its 800V DC architecture - Vertiv, Eaton, Delta, Schneider, ABB, Siemens, and others, timed around the Rubin Ultra rollout in 2027. The incumbents are racing to ship product. Vertiv’s 800V DC portfolio is slated for release in the second half of 2026.

Here is the sentence that should make every student of supply chains sit up. At OCP EMEA 2025, Google explicitly stated that its ±400VDC datacenter specification was designed to leverage the supply chain established by electric vehicles. Read that again. The world’s hyperscalers are deliberately architecting their power systems around components, voltage classes, and safety engineering that the EV fast-charging industry has already industrialised.

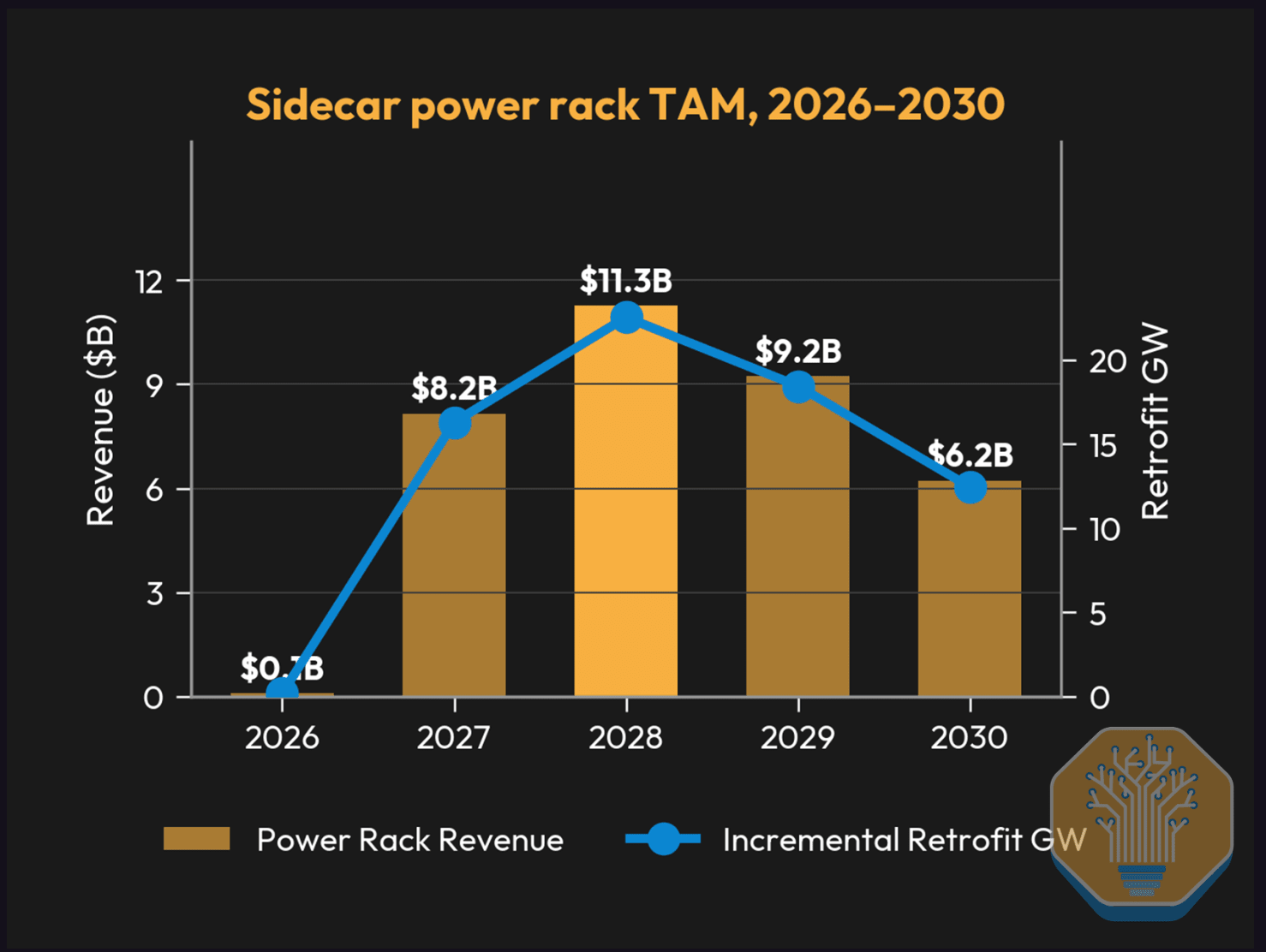

Here are some stats on how this market can progress further: 20 GW of capacity in the next two years, peaking at ~11 bn$ in 2028.

In case you want to read in detail about the trend, here is the link

Who has spent the better part of a decade industrialising exactly that?

When I first correlated Tritium’s capabilities against the 800V DC datacenter stack, the honest conclusion was: technically adjacent, commercially absent. An EV fast charger and a datacenter power shelf are cousins, not twins. Plus, every public Tritium communication through mid-2025 was about fleet charging - TRI-FLEX, NEVI, charge point operators. The datacenter word did not appear.

Can a company that builds EV fast chargers genuinely cross over into AI datacenter power infrastructure — or is this another adjacency story that dies in a slide deck?

GRID-FLEX: the product that can make inroads

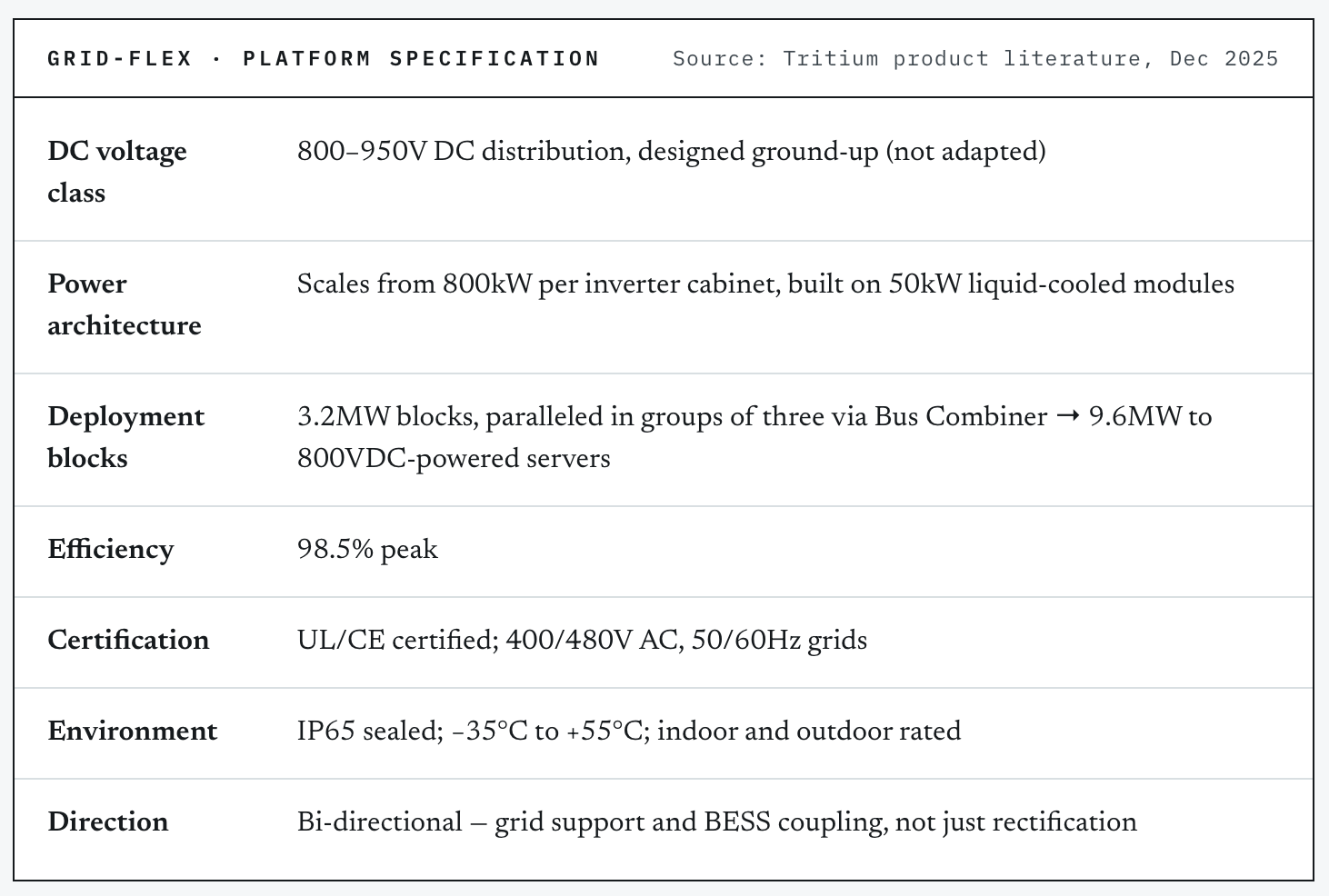

In December 2025, with minimal fanfare, Tritium launched GRID-FLEX, a high-power, grid-connected, bi-directional inverter designed from the ground up for 800–950V DC distribution, targeting datacenters, utility-scale renewables, and battery energy storage.

Tritium has been designing, manufacturing, and supporting commercial fleets of 950VDC distribution systems since 2018 - its fast chargers run exactly this voltage class on the internal DC bus, with DC distribution runs spanning up to 100 metres. The safety architecture that 800V DC datacenters require arc-fault detection, fault isolation, impedance management, DC protection coordination.

Incumbent UPS makers are approaching 800V DC from the AC world, downward. Tritium is approaching it from high-voltage DC, sideways. In power electronics, the second path is shorter.

One module, two markets: the capital efficiency story

GRID-FLEX is built on the same 50kW liquid-cooled power modules as the TRI-FLEX fleet-charging hub. This single fact carries the economics of the whole thesis:

No separate power-module development cost for the datacenter product line.

The Tennessee factory builds GRID-FLEX on the same lines as TRI-FLEX — and Hyderabad now manufactures the same modules locally, creating a second, lower-cost node.

Volume learning on EV charging directly reduces unit cost for datacenter power, and vice versa. Two demand curves, one cost curve.

This is, physically, the EV-supply-chain-to-datacenter bridge Google described at OCP EMEA 2025.

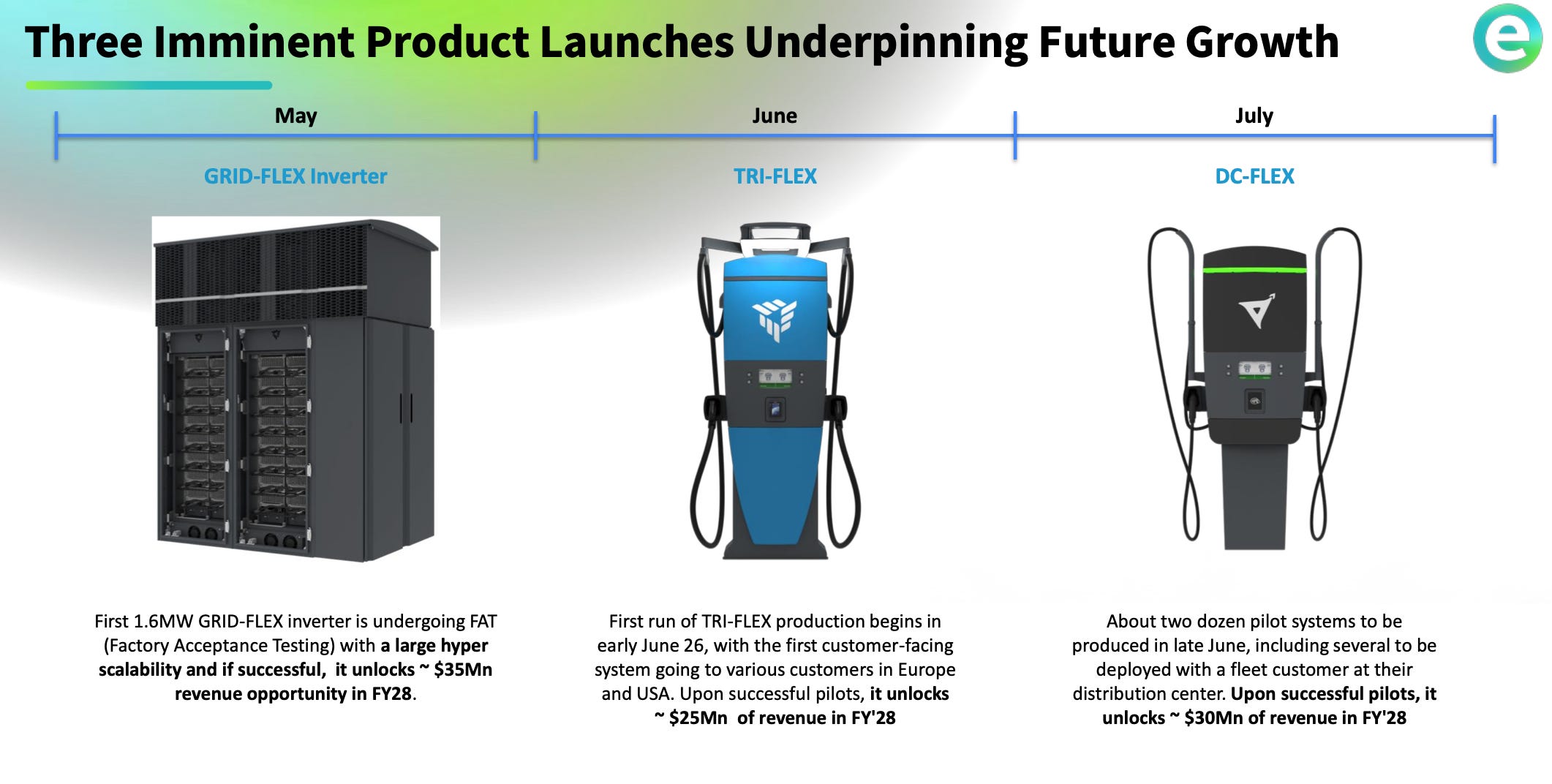

3 New products

The Q4 FY26 investor presentation quantifies three imminent product launches with a combined ~$90Mn FY28 revenue potential. The press release frames GRID-FLEX more conservatively at ~$30Mn from 2027; the deck pegs it at ~$35Mn for FY28. Either way, it is the largest single line — and the furthest along commercially, because FAT means a customer is already testing physical hardware.

The hyperscaler dynamic is what makes the GRID-FLEX a non-linear optionality. A single Factory Accepatance Testing (FAT) approval is the gate to a multi-site, multi-year procurement motion.

That said qualification is a binary event - the optionality may not work as well!!

Disc: Do your own Due Diligence. This is not investment advice

Invest in yourself…. be a learning machine.

These communities have helped me learn the nuances of investing. Why not check them out? - Join the community of learners.

Make your stock scanning easy with ChartsMaze

Supporting my work

This Substack will never be paywalled. I don’t want to accept voluntary payments for future unknown work.

But if you got this far, chances are you find my writing valuable. So please spread the word! Sharing, liking, and commenting all help spread the word!

Connect on X @pankajgarg_ciet

Disclaimer: Views are personal. I am not SEBI registered. The information provided here is for educational purposes only. This is not buy or sell advice. I will not be responsible for any of your profit/loss based on the above information. Consult your financial advisor before making any decisions.

Very Well Covered. Have written a Piece on it as well https://karanshah137.substack.com/p/exicom-tele-systemss-1400-crore-secret?r=1n1rf4&utm_campaign=post-expanded-share&utm_medium=web