Energy Transition #12 - Powering Data Centers

"Behind the Meter" powering of data centers

TLDR

Data Center growth fueled by AI (especially in the US) is scrambling for power sources. The grid can’t keep up with power requirements, forcing hyperscalers to generate electricity on-site, also known as Behind-the-Meter (BTM) projects.

Renewable (Solar/wind) typically requires a huge landmass (1 GW data center campus need ~40,000 acres given ~10 acres per MW and a solar capacity factor of 25%.), Nuclear is also looked as an alternative (again time consuming).

Hyperscalers are very sensitive to the timelines for implementation. Two technologies are competing for the BTM market - i.e., Gas & Solid Oxide Fuel Cells (SOFC) - luckily both have credible proxies in India to participate in this boom.

"The biggest issue we are now having is not a compute glut, but it's power and the ability to get the data centre builds done fast enough close to power."

Satya Nadella, CEO, Microsoft

Dear Learners,

When the CEO of the world’s most valuable company says his biggest problem is electricity — not chips, not software, not regulation — it is worth pausing and asking: what exactly is happening? And more importantly, who profits from solving it?

Today’s post is about Behind the Meter (BTM) power — a structural shift in how the world’s largest data centers are being powered.

During a gold rush, sell shovels!!

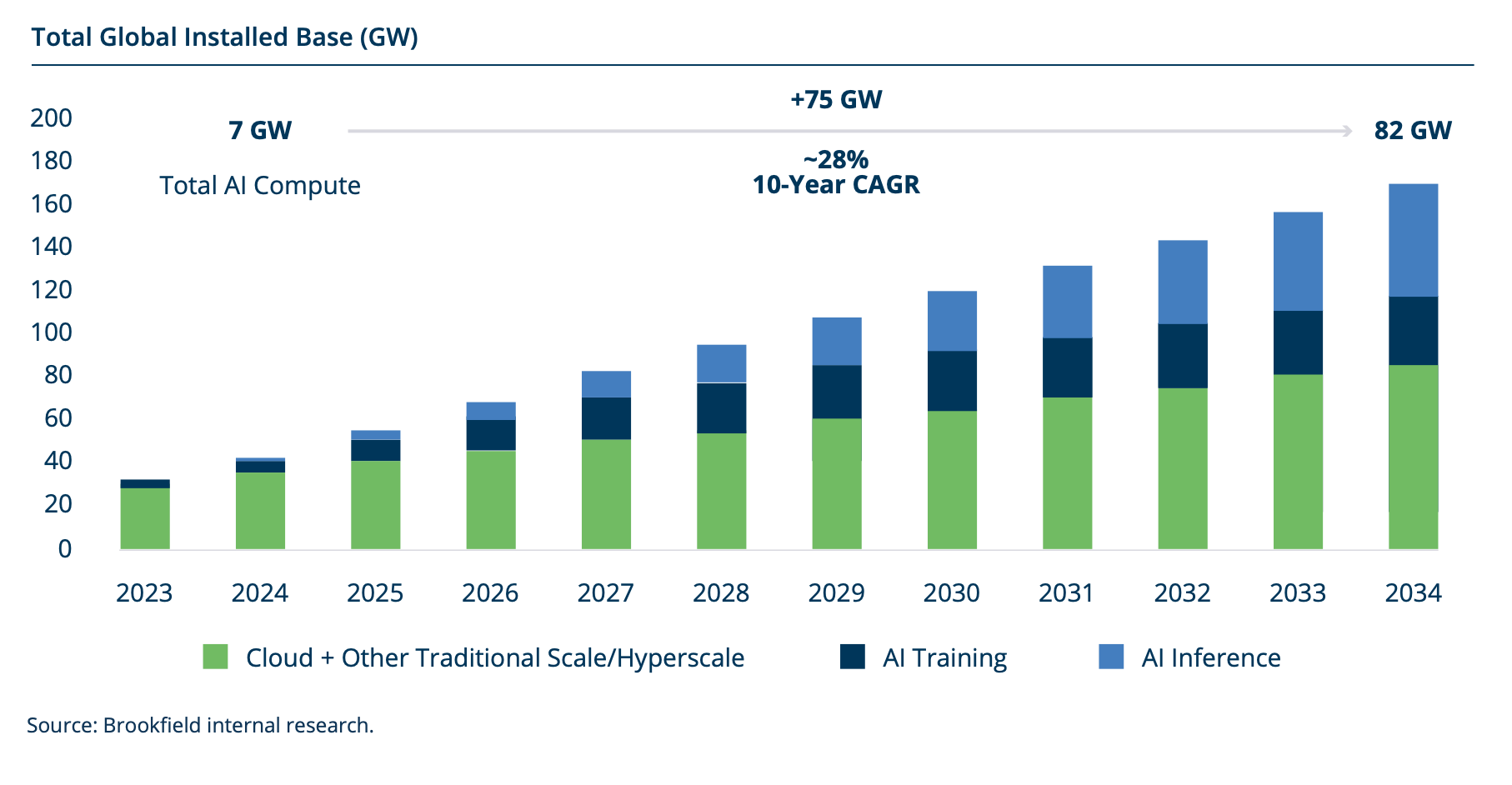

The unsatiable Power Demand

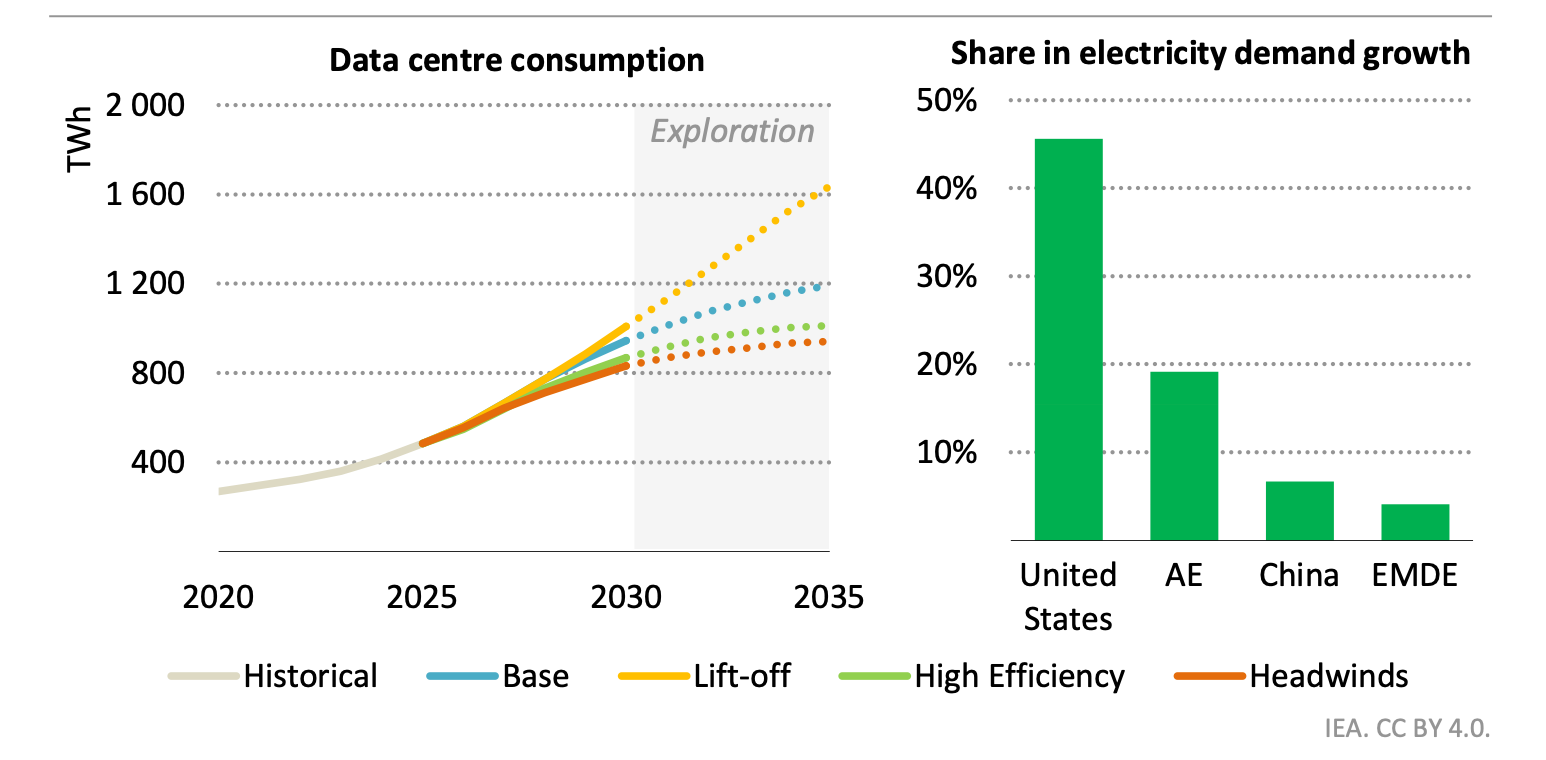

US data centers consumed 176 TWh of electricity in 2023. By 2028, that figure is projected to reach 325–580 TWh — roughly 6–12% of the entire US electricity supply. Installed data center capacity sits at ~80 GW today and is expected to reach 150 GW by 2028.

Data Center accounts for 40-50% of electricity demand growth in United States - putting tremendous pressure on the hyperscalers to power their datacenters.

Every major hyperscaler is building at maximum speed. Microsoft, Google, Amazon, Meta, and Oracle collectively pledged over $400 billion in AI infrastructure capex in 2025. New data center campuses are being announced in Northern Virginia, Texas, Ohio, Illinois — anywhere with land, labour, and fibre.

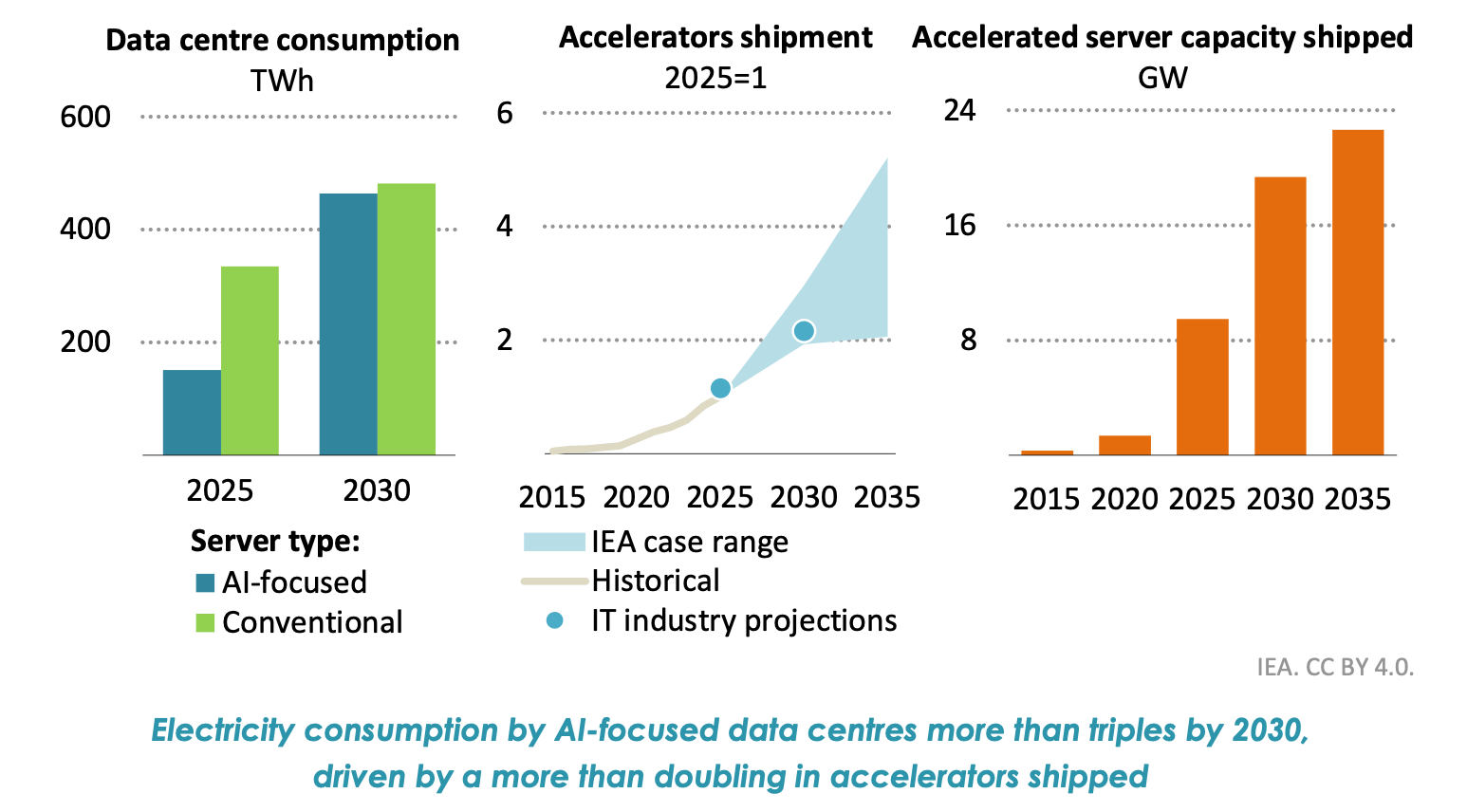

Training GPT-4 consumed 50 GWh of electricity from a single model training run. Enough to power San Francisco for three days.

Imagine the power required for upcoming models!!

The Jevons Paradox: More efficient AI will spur demand for more AI

Falling unit prices, enabled by greater scale and efficiency, can spur even higher consumption. By 2030, training a frontier model could require 10^29 FLOPS and 4 – 16 GW of power

Computational intensity is outpacing efficiency improvements…period

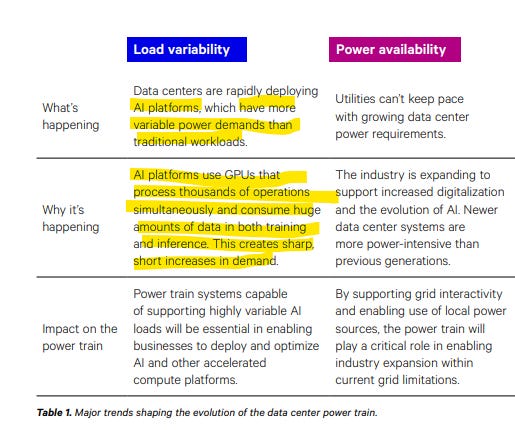

The US grid cannot keep pace with data center demand

We have written about transmission in the past as well. Integrating intermittent renewables puts immense pressure on the grid, and the demand from data centers is taking grid vulnerabilities to another level:

Al data centres see repeated swings of server load of more than 50% of rated capacity within a second.

In the year 2000, connecting a new power consumer to the US grid took roughly 22 months fast forward 2026, the median interconnection wait time has stretched to 54 months. In Northern Virginia — "Data Center Alley," home to more data center capacity than anywhere else on Earth — wait times for connections above 90MW have increased to 4 - 7 years.

Large data center load additions have a significant impact on other customers as well. It results in higher transmission costs, higher energy market prices, and higher capacity market prices.

The grid was simply never designed for this. Building new transmission lines takes 10–20 years. Adding generation capacity through regulatory approvals takes 5–7 years. But hyperscalers need power in months — because their competitors are building right now and AI market share waits for no one.

Faced with a grid that cannot respond fast enough, the world’s largest technology companies have stopped waiting for the grid and are building power plants of their own.

This is what “Behind the Meter” means. On-site generation. Your own power plant. Your own fuel supply. No utility interconnection queue. No regulatory bottleneck. Power generated where it is consumed.

Going Behind the Meter

56 GW of Behind the Meter (BTM) power projects — generating electricity on-site — were announced in 2025 alone. Oracle signed a 2.8 GW SOFC deal with Bloom Energy. Microsoft signed a 1.4 GW off-grid gas deal.

The 2025 Announcement Wave

Scale: 56 GW of BTM power capacity was announced for US data centers in 2025 alone. 90% of these projects were announced in a single calendar year.

Oracle: Signed a 2.8 GW SOFC deal with Bloom Energy — the largest single fuel cell procurement in history.

Microsoft: Signed a 1.4 GW off-grid gas-powered data center deal in West Virginia. Also restarted the Three Mile Island nuclear plant for 835 MW.

Meta: Building Ohio campus with on-site natural gas generation (Williams pipeline partnership, ~$1.6B).

White House Pledge (March 2026): Microsoft, Google, Amazon, Meta, Oracle collectively committed to “build, bring, or buy” their own electricity for new AI data centers.

Powering Behind the Meter

Two technologies are competing for the BTM data center power market and they couldn’t be more different in their approach, their economics, and their timelines.

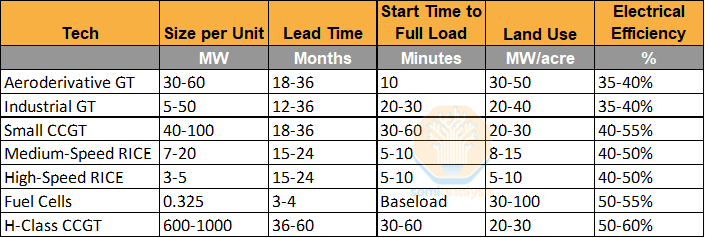

Gas Turbines: Mature, proven, manufacturable at scale. GE Vernova’s LM2500XPRESS aeroderivative turbine produces 35 MW per unit, can be deployed in as little as two weeks (95% factory-assembled), and sits on a supply chain that has served aviation and power for 50 years.

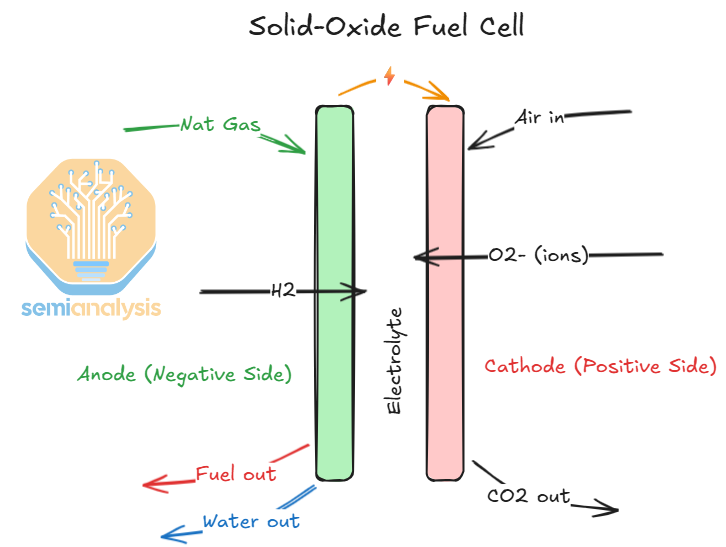

Solid Oxide Fuel Cells (SOFC): Electrochemical rather than combustion. Bloom Energy’s fuel cell servers convert natural gas to electricity without burning it — at 54–60% electrical efficiency, versus 35–42% for a simple-cycle gas turbine. Modular, silent, near-zero criteria pollutants. Deployable in 90 days.

The question for investors and the honest question for anyone tracking this space — is: which technology wins the BTM market, and what does that mean for the companies supplying them?

Gas Turbines

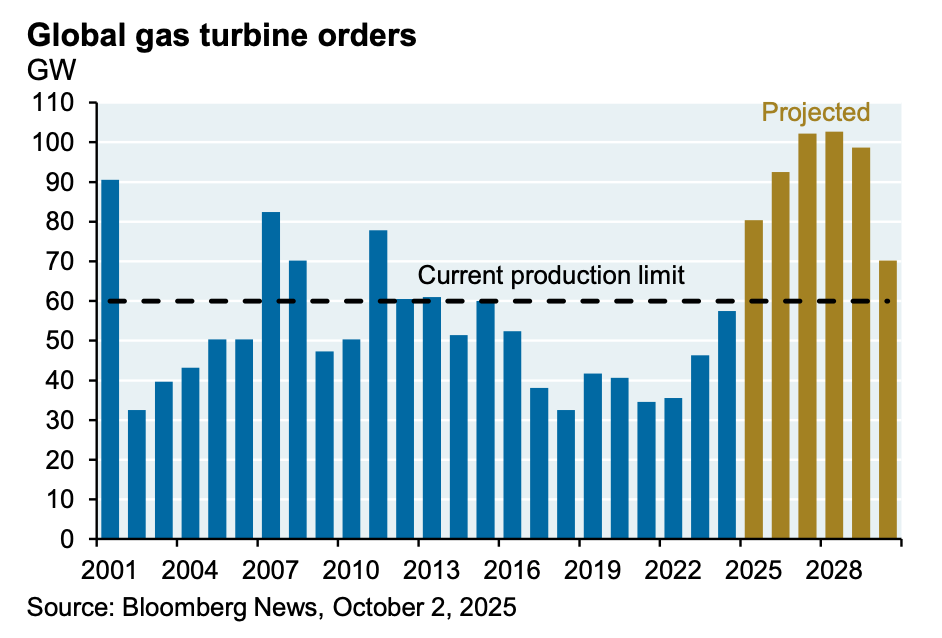

The global turbine market is currently dominated by a trio of major players—GE Vernova, Siemens Energy, and Mitsubishi. Each command a 20% to 25% market share. All three are aggressively scaling their operations to meet rising demand.

Mitsubishi intends to double its manufacturing capacity over the next two years.

GE Vernova is planning a phased expansion. Expect to increase annual output from 16 GW (2023/2024 levels) to 22 GW by the end of 2026, eventually reaching 26 GW by mid-2028.

Siemens Energy, focusing on the American market, is injecting $1 billion into US-based facilities, to boost its large turbine production by roughly 20%.

read more:

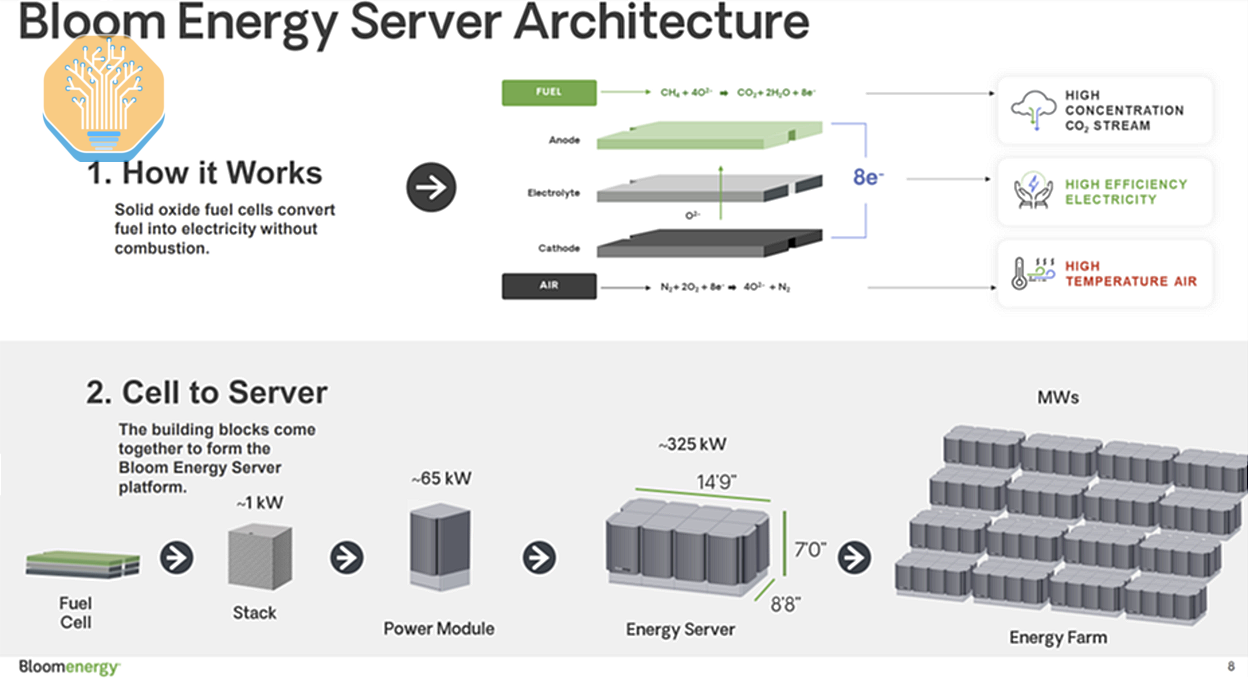

Solid Oxide Fuel Cells (SOFC)

Bloom Energy’s solid oxide fuel cell uses natural gas to produce electric power and competes with open-cycle small gas turbines and gas engines.

SOFCs do not burn natural gas to produce energy. It is an electromechanical process where fuel cells induce gas and air to interact with specialized solid ceramic materials at high temperatures, and a series of chemical processes converts the gas into CO₂ and electricity.

Faster to deploy (relatively)

Bloom Energy’s solid oxide fuel cells, once marketed with 90-day deployment timelines, now require 16-18 months for delivery, installation, and commissioning of 50+ MW installations

A niche in the sector

Current global generation of ~7 TWh per year from ~1 GW of installed fuel cells; that’s just 0.02% of global electricity generation

Increasing Deployment

Bloom -Oracle (2.8 GW) and Bloom Brookfield ($5 billion) are examples of increasing acceptability and deployment

To sum up

Thirst for data center power is reaching unprecedented levels. Physical constraints are limiting the rate at which data centres can be built. This is clearly a suppliers market.

Coming up next - Indian companies in the value chain.

Sources:

Fighting Worlds - JPM 16th Annual Energy Paper

Invest in yourself…. be a learning machine.

These communities have helped me learn the nuances of investing. Why not check them out? - Join the community of learners.

Make your stock scanning easy with ChartsMaze

Supporting my work

This Substack will never be paywalled. I don’t want to accept voluntary payments for future unknown work.

But if you got this far, chances are you find my writing valuable. So please spread the word! Sharing, liking, and commenting all help spread the word!

Connect on X @pankajgarg_ciet

Disclaimer: Views are personal. I am not SEBI registered. The information provided here is for educational purposes only. This is not buy or sell advice. I will not be responsible for any of your profit/loss based on the above information. Consult your financial advisor before making any decisions.